Is Life Insurance Taxable? (Guide for Canadians)

Is life insurance taxable in Canada?

In the majority of cases, life insurance payouts are not taxable in Canada – regardless of whether it’s a term, permanent, whole, or universal life insurance product..

When it’s not taxable: When the insured person passes away, the death benefit is paid out to the named beneficiary as a tax-free lump sum. There is no death tax or estate inheritance tax for beneficiaries to pay.

When it might be taxable: The exception is if a payout accumulated interest, was paid out to an estate, if there was investment income, or if cash value was withdrawn as a policy loan. These count as income.

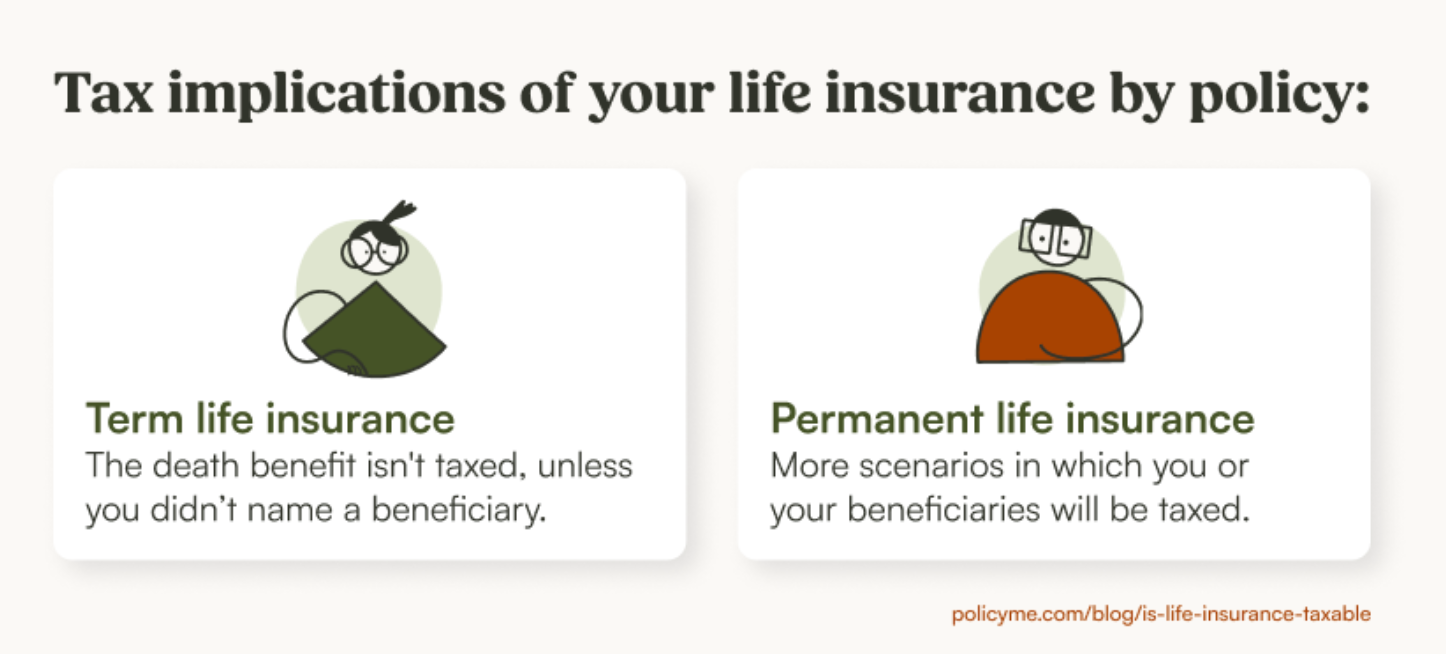

Here’s a simple breakdown of taxability:

Anything outside of your life insurance payout could be taxed—for example, if you withdraw money prematurely from your policy's cash value (more on that in the next section):

For both term and permanent life insurance, if you fail to name a beneficiary, the death benefit may be subject to probate.

When is life insurance taxable in Canada?

Life insurance is taxable in Canada in two situations:

- Taxable when it’s considered income, like cash value policies

- Taxable when it becomes subject to estate taxes via probate

This is why death benefit payouts are typically tax-exempt—they are not considered income.

The tax implications of a life insurance policy change depending on which type of life insurance you buy: term or permanent.

- Term life insurance death benefits aren't taxable in Canada, unless your policy doesn't have a named beneficiary. In this case, the payout may be subject to probate.

- Permanent life insurance policies, such as whole life and universal life, may have tax implications, like paying tax on a withdrawal of the cash value.

Here’s a comprehensive overview of when life insurance is taxable for Canadians:

- You don't name a beneficiary in your life insurance policy. Probate may then apply.

- You withdraw from the cash value of a permanent life insurance policy and it exceeds your adjusted cost basis.

- Your policy lapses with an outstanding loan; the loan amount may be taxable.

- You cancel your permanent policy (in some cases).

- Your beneficiaries get interest earnings from your policy after your death.

- You sell your permanent life insurance policy while you're still alive.

You don’t name a beneficiary

If you don’t name a beneficiary, your life insurance payout defaults to your estate, which can create probate and administrative issues. Here’s what happens when your estate is the beneficiary:

- The payout becomes part of your overall estate assets.

- Those assets are distributed according to your will.

- The estate may owe probate before funds are passed on.

Reviewing your beneficiaries regularly and updating them as necessary helps ensure your payout goes directly to the people you choose, not the provincial or territorial government.

You withdraw from the cash value or take a loan

Under Canada’s Income Tax Act, life insurance death benefits are generally excluded from taxable income, with a notable exception: permanent life insurance policies can build cash value that grows on a tax-sheltered basis while it stays inside the policy. Taxes may apply if you withdraw or borrow against that cash value.

The CRA uses something called the adjusted cost basis (ACB) to determine how much of a withdrawal or surrender is taxable. If you withdraw or surrender funds and part of the amount exceeds your ACB, that excess is treated as taxable income. Your insurer will issue a T5 slip for the taxable portion.

ACB = total amount contributed to policy (premiums) - cost of insurance +/- any adjustments (e.g., loans, dividends, riders, or changes in insurance coverage)

For example, let’s say you’ve paid $30,000 in premiums, and your policy’s cost of insurance was $5,000. Your ACB will be $25,000, with no additional adjustments. If your cash surrender value is $30,000, your taxable amount will be $5,000, and your insurance provider will send you a T5 slip that highlights the applicable tax.

Withdrawing or borrowing from a life insurance policy can be complex, so it’s best to consult a licensed financial professional before accessing your cash value.

Surrendering (cashing out) a permanent policy

Cancelling a permanent life insurance policy—also called surrendering or cashing it out—can trigger taxes. While your policy is active, its investments are tax-sheltered. But once you surrender it:

- Any cash value above your ACB is taxable.

- The taxable amount is treated as income, not a capital gain.

You earn interest on the death benefit (if applicable)

Life insurance death benefits themselves are tax-free, but interest earned on those benefits may be taxable. This can happen when:

- There’s a delay in paying out the death benefit and the insurer pays interest during that period.

- A beneficiary chooses an interest income option, where the insurer holds the payout and pays interest over time instead of issuing a lump sum.

In these cases, the principal death benefit remains tax-free, but any interest earned is considered taxable income and must be reported to the Canada Revenue Agency (CRA).

You sell your permanent life insurance policy

Selling a life insurance policy while you’re alive is currently only legal in Quebec. If you sell your policy:

- Any gain from the sale is treated as taxable income.

- You must report the income to the CRA and Revenue Quebec.

It's currently illegal to sell your permanent life insurance policy in most provinces and territories in Canada. While it used to be legal in New Brunswick, Nova Scotia, and Saskatchewan until 2020, it is now only permitted in Quebec. There is a movement in Ontario to make it legal under Bill 219, which would allow Ontario residents with life insurance to sell their policies.

You transfer your policy

Transferring ownership of a life insurance policy can also create tax consequences. Transfers to a spouse or qualifying trust are usually tax-free. Transfers to anyone else, including a corporation you own, may trigger taxes, especially if there is a cash value.

Special note: Employer-paid group life insurance premiums

If you have group life insurance through your employer, the death benefit is still usually tax-free; however, the premiums that your employer pays may be considered a taxable benefit to you as an employee. In those cases, the value of the premiums may be added to your taxable income and reflected on your T4 slip.

Is life insurance tax deductible in Canada?

Life insurance premiums are generally not tax deductible in Canada under CRA regulations. This means that you generally can't deduct the premiums paid on a life insurance policy from your taxable income.

There are some exceptions to this rule:

- Business relations: When a life insurance policy in Canada is used for business purposes, the premiums may be tax-deductible as a business expense.

- Loan collateral: When a life insurance policy is used as collateral for a loan, the interest paid on the loan may be tax-deductible.

The tax rules regarding life insurance can be complex and may depend on factors such as the type of policy, the purpose of the insurance, and the tax laws in your specific province or territory. Consult with a qualified tax professional if you have questions.

What is the tax rate for life insurance in Canada?

There isn’t a fixed tax rate for life insurance in Canada. Life insurance death benefits are generally tax-free when paid out directly to a named beneficiary.

Taxes typically come into play when you:

- Withdraw from your policy’s cash value

- Surrender your policy

- Earn taxable interest on a deferred death benefit payout

- Invest life insurance proceeds once received

In these cases, the portion income may be taxed at your marginal tax rate—the same rate you pay on other types of income.

Tax benefits of life insurance

In general, the biggest benefit of all life insurance policies is the tax-free lump sum payout that your beneficiaries receive when you pass away. The CRA does not tax this benefit, so your loved ones can use it however they see fit—often to cover final expenses, pay off a mortgage, or replace your income.

To top it off, here are the most noteworthy benefits of life insurance:

- Cover your estate’s tax bill: When you pass, your estate (including a cottage or RRSPs) may incur a hefty tax bill. Your life insurance payout can be used to cover these taxes, ensuring your estate stays intact for your family and beneficiaries.

- Skip estate probate fees: Your death benefit will go directly to your named beneficiaries, which means it won’t fall into your estate and lead to probate fees.

- Tax-free inheritances: Your policy’s payout can help provide fair inheritances to your children or loved ones, and taxes won’t affect how much they receive from your death benefit.

- Tax-deferred growth: Permanent policies build cash value, which is tax-deferred and can be withdrawn up to your adjusted cost basis without tax consequences during your life.

Term life insurance is the most affordable way to secure a tax-free death benefit for your loved ones. It will have the lowest premiums. While it doesn’t include an option to build cash value, it balances the value of life insurance and provides ample protection for your family and beneficiaries during the most crucial years.

Life insurance policies do not affect your income, so they cannot affect your final tax return. While permanent policies may have a tax-deferred growth component, and you may be able to borrow against it, it’s never tax-free. You also sacrifice flexibility, pay fees, and lose out on higher growth through other tax-advantaged accounts like TFSA and RRSP.

Can I use life insurance to reduce tax on my final tax return?

You can’t technically reduce the amount of tax owed on your final tax return. Your taxable income, tax deductions, and tax credits in the year you die determine that amount; however, life insurance can help you cover your final taxes by providing your loved ones with a tax-free lump-sum payout after you pass away.

That payout can then be used to pay things like:

- Income tax owed on your final return

- Debts you owe

- Other estate-related expenses

To make this work, you need to:

- Name your beneficiaries on your life insurance policy, so the payout doesn’t end up going to your estate (which could lead to probate fees)

- Make sure your will is up-to-date and appoints an executor

While life insurance doesn’t reduce the tax you owe when you die, it can still play a role in tax-efficient estate planning by providing liquidity when it’s needed most.

If tax advantages and long-term value are important to you, then term life insurance offers the highest value for the average Canadian family, as you can see from the price breakdown below.

PolicyMe offers some of the most competitive term life insurance rates in Canada, with an easy online term insurance calculator to help you assess your needs.

FAQ: life insurance and taxation in Canada

Jaya is a researcher and writer with 3 years of experience in insurance and finance. She writes in-depth content that bridges technical expertise with accessible insights. Her work spans topics such as life insurance, health and dental coverage, car insurance, and financial literacy, helping Canadians make informed decisions about their financial protection. With a background in market research and editorial strategy, she collaborates closely with subject matter experts to ensure accuracy, clarity, and value in every piece.

Jaya is a researcher and writer with 3 years of experience in insurance and finance. She writes in-depth content that bridges technical expertise with accessible insights. Her work spans topics such as life insurance, health and dental coverage, car insurance, and financial literacy, helping Canadians make informed decisions about their financial protection. With a background in market research and editorial strategy, she collaborates closely with subject matter experts to ensure accuracy, clarity, and value in every piece.